State of the EV Market: Five Key Trends

.avif)

Corey Cantor

The ZETA team recently attended New York Climate Week, and as part of one of our events, I crafted a short presentation on the state of the EV market. Following the week’s events, I believe it would be worthwhile to share these insights with all our readers who may want to calibrate their understanding of where electric vehicles stand, both globally and in the United States.

There can be a lot of noise in the market, due to complicated messaging, painting things in a more pessimistic or optimistic light than might otherwise be warranted. Focusing on some big picture items could help reset perceptions of the EV market as we enter a new phase. The EV consumer tax credit has just expired, with news sources indicating record sales for the past three months, and there is a high likelihood that the next few quarters may see a slight correction as the market adjusts to the new policy reality.

Still, this year is one chapter in the overall story of the U.S. auto market. So with that, let’s discuss five key trends that illustrate the current status of EV adoption.

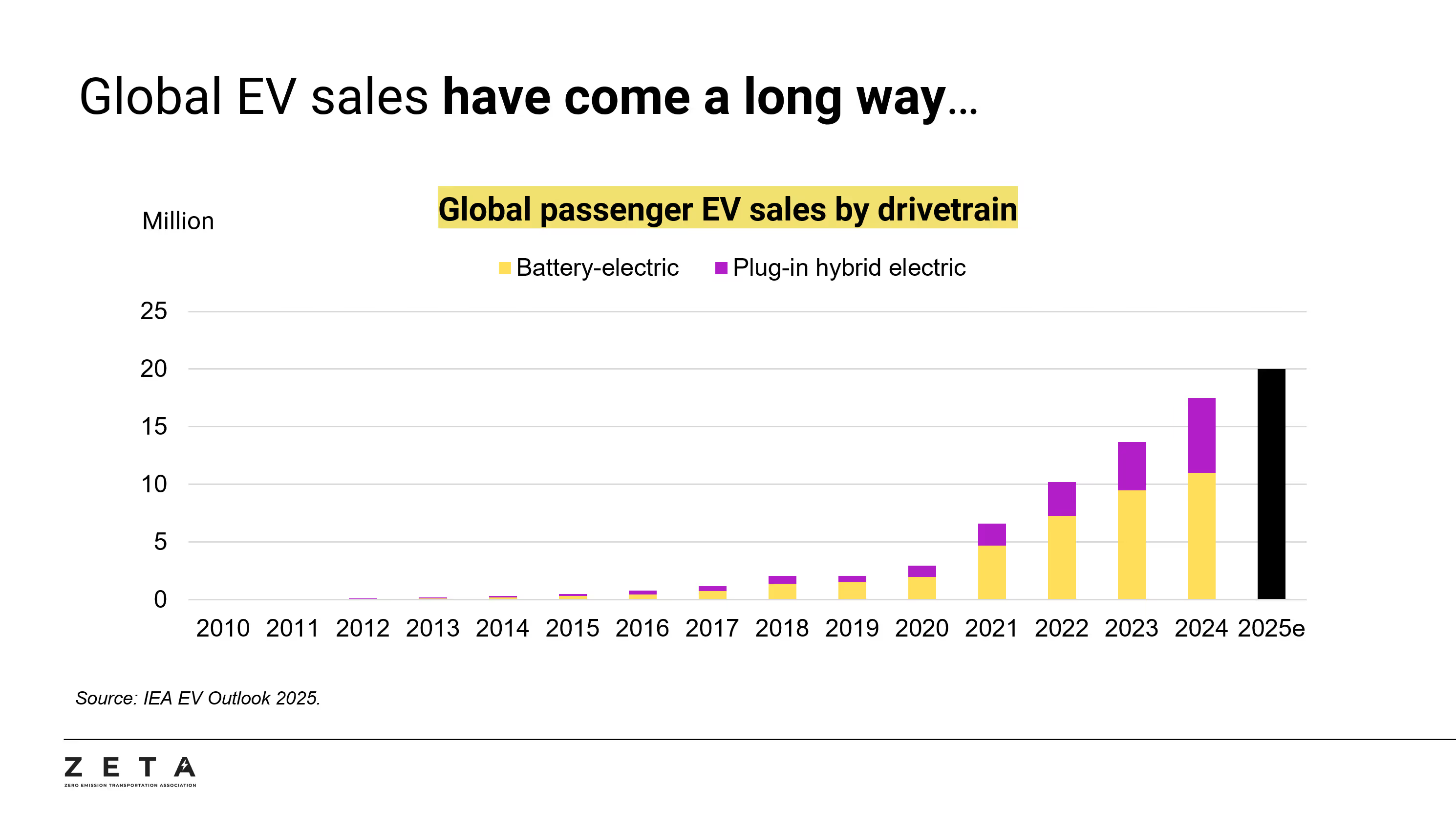

#1: EV adoption has come a long way

If you were reading a story or blog about electric vehicles in 2015, you’d see that they barely made a blip on a chart. That year, worldwide EV sales accounted for around 500,000 units, according to the International Energy Agency (IEA). Ten years later, EV sales are on pace to grow by forty-times, reaching an estimated 20 million units sold worldwide in 2025 under IEA’s latest forecast.

We have also seen immense growth in the U.S. market. In 2015, electric vehicles made up 0.70% of the market. At that point, only the Tesla Model S was a notable model on our shores. Fast forward to 2024, and EVs represented 10% of new car sales according to the IEA. Over that period, battery-electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) grew at a compound annual growth rate (CAGR) of 42%, which is impressive. We’ve covered that point previously, but it’s undeniable that these alternative drivetrains—along with conventional hybrids—represent a key growth segment in the U.S. auto market.

#2: Lower cost EV batteries has been the driving macrotrend

Given that batteries represent anywhere between 30% and 50% of an electric vehicle’s cost, the decrease in the cost of lithium-ion battery pack prices has brought EVs from a niche product to one that has gone mainstream. BloombergNEF’s battery price survey found that pack prices globally fell to $115 per kilowatt-hour (kWh) in 2024, down 20% year-on-year. This is a far cry from the prices in 2010, which were nearly $1,400 per kWh. With tariffs and supply chain disruption, it will be interesting to see if this year will see further declines. BloombergNEF typically releases its survey towards the end of each calendar year.

#3: The U.S. EV market must go back to basics

Following the passage of the One Big Beautiful Bill Act (OBBBA), many have asked where the private sector and other stakeholders ought to focus in regards to the EV market. Surveys suggest that it is key to go back to basics in order to address perceived barriers to entry to EV adoption.

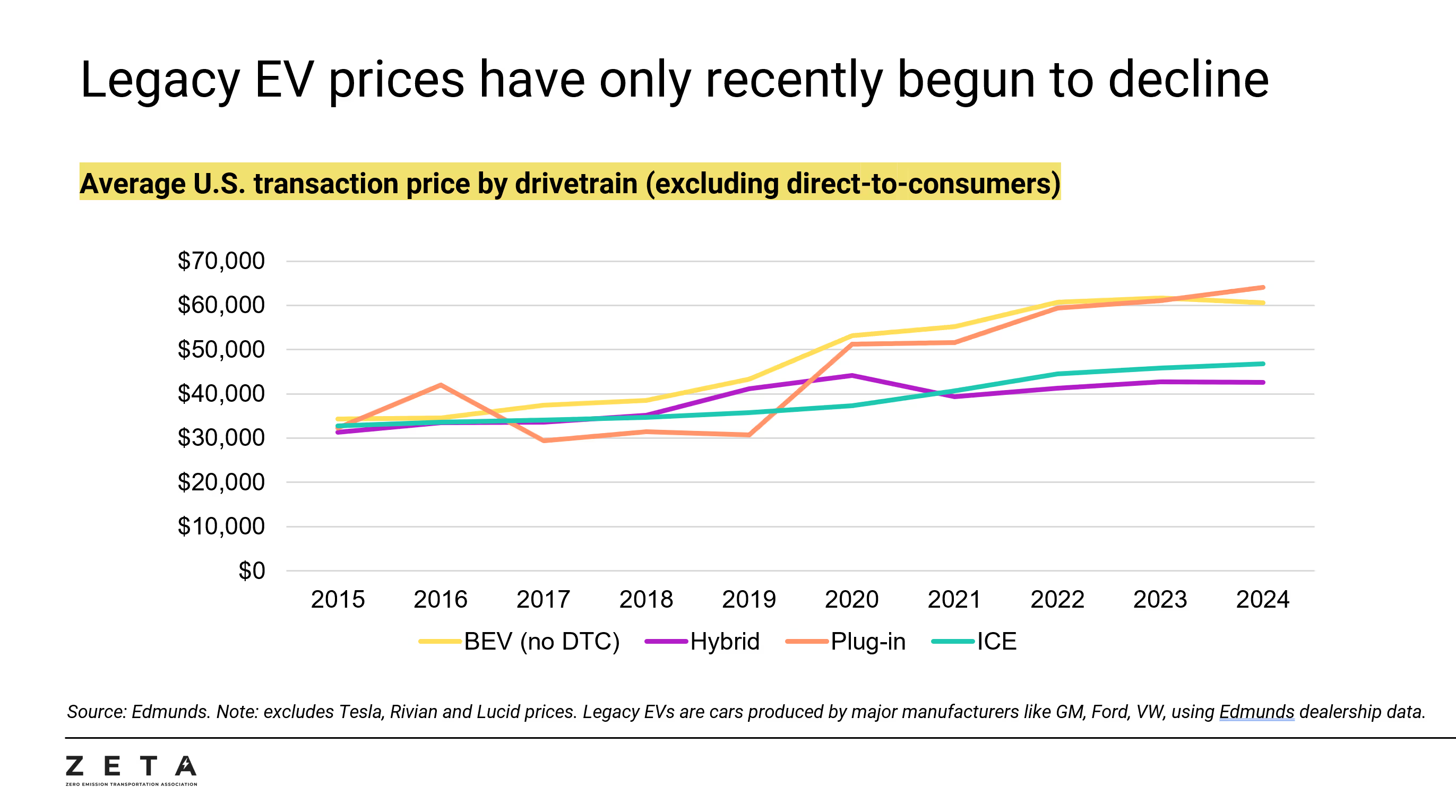

In the U.S., two recurring concerns for prospective customers remain the upfront cost of electric vehicles and a perceived lack of charging infrastructure. On upfront cost, price parity remains a couple of years away for most vehicle segments. However, this past summer saw some interesting developments in the market.

Data from Edmunds highlights how the EV leasing incentive (45W tax credit) helped the average monthly cost of owning an EV drop below the average of a gas car - especially as vehicle costs have come down over time. Due to the leasing credit, as well as the now-expired 30D consumer tax credit counterpart, more drivers were exposed to electric vehicles, ensuring that automakers and battery manufacturers had demand for their product as they scaled up operations to ultimately bring manufacturing costs down.

Though this tax benefit will now disappear, new more affordable models coming over the next year could make a critical difference in securing this trend long-term, including vehicles like the Rivian R2, Kia EV3, the returning Chevrolet Bolt, and more. The average price of EVs made by legacy automakers have only recently begun to decline.

On charging, the private sector has stepped up, leading to what the analysis group Paren suggests might be a record year of EV charging installations. With new guidance issued around the National EV Infrastructure (NEVI) program, there are potentially positive tailwinds heading into 2026 and beyond. 40 states are now in the process of unlocking funds for EV charging following the re-opening of the program. Given that consumers continue to have questions about charging availability, it remains a task that the industry can tackle together in the near term.

#4: China’s rise is multi-faceted and critical to acknowledge

It’s important to acknowledge that the rest of the world continues its rapid movement towards electric vehicles. In China, EVs are making up nearly half of monthly sales, amidst ever- increasing competition. Furthermore, China is rising compared to its competitors globally.

In 1999, China represented 1% of all global passenger car production, according to the International Organization of Motor Vehicle Manufacturers (OICA). That same year, the U.S. represented 14%. Flash forward to 2023, China’s share ballooned to 38%, while the U.S. production share fell to 3%. This is not just about electric vehicles, but about all cars.

Similarly, China has played a significant role in carving out control over the battery midstream supply chain, including cathode and anode production. China’s share of production has generally represented between 80% to 95% of global manufacturing capacity for each battery component and cell manufacturing. Much of U.S. policy over the past five years, including the 45X tax credit, has aimed to onshore more battery manufacturing to make a dent in China’s lead in batteries.

#5: Federal policy has weakened, but interest in the sector continues

There’s no denying that it has been a chaotic few months in the industry, culminating in the passage of OBBBA and the rollback of several EV-supportive policies.

But one takeaway from Climate Week and an important message is that D.C. doesn’t have the last word when it comes to market preferences. Consumers, industry, advocates, state policymakers, and other stakeholders have a major role to play in this story too.

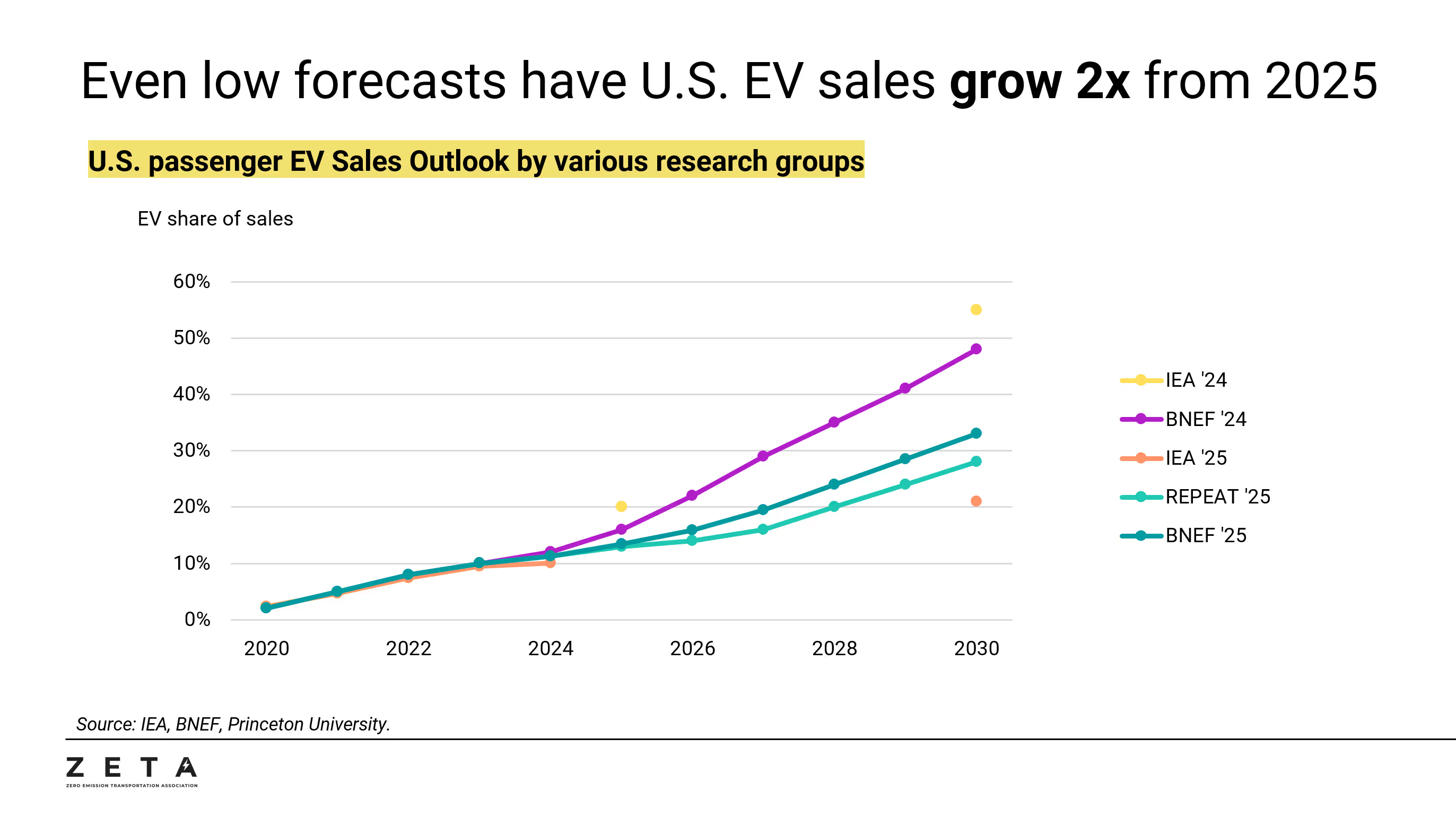

Consider this: while market research groups have downgraded their previous projections for EV growth in the coming years, the EV market is still projected to double 2025’s outlook by 2030.

If there’s one final takeaway from this current moment to keep in mind, it’s that each day more and more consumers are going electric. And the industry that produces them - from upstream of critical minerals producers to downstream recyclers - is only growing stronger with each given day. The road ahead remains a long one, but each of us has a part to play.