From Early Challenge to Rapid Expansion – The Evolving EV Charging Landscape

.avif)

Corey Cantor

The U.S. charging network is in the midst of a massive transformation that will leave EV owners and future drivers far better off. Concerns around EV charging are commonly rated among the foremost barriers to EV ownership. Deloitte's 2026 Global Automotive Consumer Study found that three of the top five concerns regarding battery-electric vehicles were all related to infrastructure: range anxiety, EV charging speed, and the number of charger locations.

Ultimately, what consumers want is access to charging infrastructure that is expansive, reliable, and fast. The data shows that there are clear, positive trends to share on all three counts. Recently, we spoke with Bill Ferro of Paren, who highlighted how much the EV charging experience has improved.

More Expansive

The public EV charging network shows strong signs of growth. Since 2021, the network has more than doubled, reaching nearly 245,000 connectors as of the end of March 2026, according to data from the Department of Energy’s Alternative Fuels Data Center.

Of those connectors, around 70,000 of them are fast-chargers (DCFCs), which make EV road trips easier and speedy public charging more accessible – 75% of the DCFC network, comprising 52,000 connectors, were built in just the past five years. The rapid growth of fast charging is private-sector driven, according to Ferro, with companies like Tesla, EVgo, Electrify America, Ionna, Red-E, and Walmart among the recent stand-outs installing chargers across the country. Fast charging installations grew by about 30% in 2025 compared to the previous year, totaling around 18,000 connectors – a sign that the private sector’s efforts are picking up speed.

Still, the expansion of EV charging hasn’t been uniform across the country. Around 25% of the network’s fast-charging connectors (and 26% of all public charging connectors, when including level 2) reside in the state of California, where EV adoption is further along. The Golden State represented nearly 30% of all EVs sold in the U.S. in 2025, while accounting for 11% of all cars sold in the U.S. last year. As the private sector focuses on areas with high utilization, rural areas have seen lower growth — evidence of the continued case for federal investments in public charging to fill gaps in the national network that aren’t currently prioritized by the private sector.

“While [the National EV Infrastructure formula program (NEVI)] was never intended to be on the leader board, it continues to fill in the spots and make that great American road trip easier and better,” noted Bill Ferro in conversation with ZETA. “You look at Pennsylvania, Wisconsin, and Minnesota – these are states that have really expanded their NEVI program this year.”

In addition to a growing number of charging station locations, the average size of charging sites is growing, too. According to data from Paren, the average non-Tesla network site now has 4.6 connectors, up from 3.4 in Q1 2025. For Tesla’s charging sites, the average number of connectors per station is around 12.

Paren’s analysis also looks at charging site utilization. When charging connector utilization is too high, the network may be strained. Conversely, too low a level of utilization may suggest an oversupply of connectors. Fortunately, the data shows that the utilization of EV charging sites has trended upwards over the past few years. Paren has attempted to identify this sweet spot on a port and station basis, identified in the figure below. “When we look at where we are at and where we’re trending towards… we’re seeing infrastructure is keeping us in that Goldilocks zone,” Bill noted when asked about recent utilization data. This is a level of charging that most charge point operators (CPOs) would want to see their stations fall within. This is a high enough level of utilization that CPOs would see strong revenues from their stations, but not so high that consumers experience major congestion and are discouraged from charging at a particular site. It’s a fine balance and one that is tricky to maintain, given that the amount of driving is significantly higher in the non-winter months.

Utilization of EV charging sessions

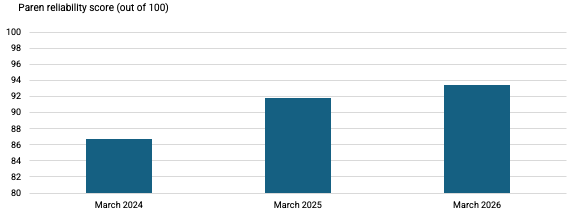

More Reliable

The overall reliability of the public EV charging network has substantially improved, though there is more to do in order to ensure reliability nationwide. When EV adopters pull up to a station expecting to be able to charge, they need to have confidence that they will not face unforeseen technical or maintenance issues that prevent them from doing so.

Bill noted that the early lack of reliability in the EV charging network was part of what encouraged him to first start tracking the network. His data firm came up with a metric for tracking the reliability of charging ports to measure the pace of improvement over time.

Overall, the average reliability score across the network has risen from 86.8 in March 2024 to 93.4 in March 2026. Still, the reliability of networks in individual states may vary dramatically from the national average. Paren suggests that improvement in reliability can be attributed to a few main factors, including the influx of new hardware on the scene, the refresh programs of several networks, and the replacement of many older, legacy stations.

More Effective

Recent improvements in the network have prompted positive feedback from both EV drivers and the press alike. Looking forward, a goal for the public charging network is not only to meet the needs of the traditional driving experience with legacy infrastructure, but find a way to surpass it. The special sauce for electric vehicles has always been the idea that charging can take many forms in many locations at different speeds. Infrastructure improvements shouldn’t just mean that long road trips in your electric vehicle will be easy, it should also mean that the day-to-day experience of owning and operating an EV will become even more enjoyable.

Increasing satisfaction in the current state of the network has been hinted at, most recently in an EV Owner Survey by JD Power, but it’s possible to think bigger about what the U.S. charging network should look like. A stronger network could mean higher charging power, an increase in the number of ports per site, and ensuring that there are no “gaps” in the network – particularly in rural areas. Industry seems to be taking these considerations into consideration over the past two years, as the competition between different charge point operators has heated up.

It’s worth keeping in perspective that we are still in the early days of U.S. EV adoption, no matter which date you choose to measure it from. It took decades for the original gasoline infrastructure for internal combustion engine vehicles years to fill out. In fact, early drivers would have to plan their trips ahead of time and in some cases ship gasoline to convenience stores along their route to ensure they have the necessary fuel. EV charging has a bit in common with those early days, including range anxiety and gaps in the network.

Over time, the ability to charge anywhere in a variety of ways, from fast charging to Level 2 and trickle charging, gives EV users flexibility that other drivetrains just don’t have. What was initially a disadvantage may soon be turned on its head. While getting there will take some time and a full-industry effort, the recent data shows that the U.S. public charging network is moving in the right direction – and quickly.